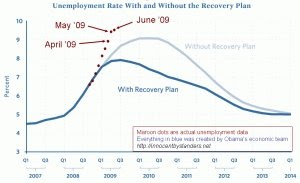

Unemployment jumped again in yesterday's

report. Them's the brown dots. What the Obama Administration promised--both pro and con--for the Stimulus plan are those two lovely curves below that steep line you see if we connect all those dots. You remember...unemployment topping out at 8.5% vs. 9%.

Well, we're at 9.5% and far more likely to blow through 10%--a number not seen since 1982--than not. What do folks have to say about it?

Well,

this is pretty self-explanatory:

Be sure to thank the President and Congress. This week, with news of some 467,000 jobs lost in June, the Bureau of Labor Statistics estimates that the U.S. has now lost about two million jobs since the economic stimulus package passed. Even more notable is that the average workweek has been slashed to 33 hours - the lowest number on record. When the President signed his $787 billion stimulus package into law, he confidently asserted that unemployment would not exceed eight percent. If Congress hadn’t passed it, he warned, it would rise to nine percent by 2010. Well, unemployment reached 9.5 percent last month, meaning, by the President’s own logic, that his stimulus package has failed.And Jennifer Rubin

pulls no punches:

We are recovering. But unemployment is getting worse. And the stimulus is definitely working. Got it? It sounds like they haven’t a clue what to do and don’t want to admit they have been concocting a disaster. And we shouldn't pick on Gibbs. The president and the rest of the administration are no better:...And what of John Q. Public? Well, how 'bout

this:

A Rasmussen video report notes that 42% now give the President good or excellent marks for handling the economy . That’s his lowest rating to date...

I expect that, and the approval ratings that go with it, will fall even further when we break 10%, assuming we do (and I feel pretty confident that's much more likely than not). At the risk of sounding like one who is just having fun switching roles from

Bush Apologist to Obama critic, I must refute such an allegation, should it come.

The hallmark of President Bush's critics over his 8 years in office, by far, was anger, mixed in with a little irrational hatred of a man 99.9% of them never met much less truly know. The final ingredient in this vile concoction was the fundamental lack of respect for all who disagreed with them about the President and his policies.

President Obama is my president; while I did not vote for him, I will support him when I think he's right, I will be critical when I think he's wrong and I will always show him the respect he deserves. I am not angry with the President over Guantanamo Bay, Iraq or the economy. I think his decisions have been incorrect, but I am not angry.

To the contrary...on the economy I'm actually laughing. I knew his proposal couldn't and wouldn't do what he was promising. I'm sad to see that we're forced now to wait out more difficulty than we otherwise would as a result of his policies. But that is where we're at.

What I patiently wait for is the Administration and it's supporters to finally acknowledge that they own what is now happening in the country. George W. Bush is no longer President; the Democrats who have controlled Congress for 3 years have made every effort at ensuring his policies are no longer in place.

To the Administration and it's supporters, man up! Own your failures. It'll make it far easier to own your successes down the line.